While this post applies to any sale where the prospect already uses a competitor's product or service (which would be almost any sale), I present the importance of "unselling" in the context of this blog, a financial sale.

Your Prospect's Unwillingness to Buy What You Recommend

Your Prospect's Unwillingness to Buy What You Recommend

Before you every give recommendations for your product or service, you must frame them so that the prospect is most likely to take them. There are two aspects to performing this successfully

- providing independent evidence why your products and services are the best solution

- providing independent evidence why your prospect's current choice of products and services must be abandoned.

Most every sales professional skips step #2 and then wonders why it is difficult to close the sale. You must realize that the prospect has an allegiance to the products and service and the providers already used. The prospect has such allegiance because of these basic psychological factors below.

Every Prospect is Unwilling to Buy for 3 Reasons

- Post-purchase rationalization. As Wikipedia states

"Post-purchase rationalization, also known as Buyer's Stockholm Syndrome, is a cognitive bias whereby someone who has purchased an expensive product or service overlooks any faults or defects in order to justify their purchase. It is a special case of choice-supportive bias."

In other words, if you purchase a Chevrolet, you will defend the purchase no matter what negative facts may come to light about Chevrolets.

- The existing relationship with the "very nice guy" that sold me the products/services creates a switching cost. In economics, a switching cost example would be an exit fee such as when you want to terminate your cell-phone contract before the term is up. But there are psychological switching costs simply because we become accustomed to certain people or processes. They become familiar and we like familiar. We have the existing advisor in our cell-phone contacts, we drive by their office on the way to the super market, we know another client they serve, etc.

- Then, we have the risk of switching. Even if the prospect dislikes or is unhappy with their current choice or products and services, we have saying in our culture, "the devil you know is better than the devil you don't know." This may explain why people stay in bad relationships and continue to drive a car that breaks down every week.

If you do not disturb these emotional reasons for the prospect to stay with a portfolio or provider that he may even complain about, you will likely not have a new client.

The Unselling Process for a Financial Advisor

Let's assume in our example that our prospect has a portfolio of mutual funds that we desire to replace.

So many mutual funds have problems; it is simple to show a prospect why the funds or managed account you offer is better. However, realize that your prospect has some allegiance to their existing holdings, as described above, even if those holding have been poor performers. The prospect's inertia to do nothing is overwhelming. Therefore, before presenting your recommendations, you must loosen their grip on their current investments.

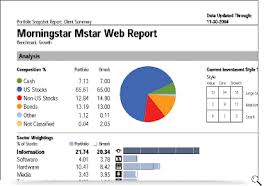

Use this technical approach. When meeting a prospect, tell the prospect you want to obtain independent reports on their current funds detailing how their funds are performing (most investors have no clue about their performance other than “up” or “down”). Then get Morningstar reports on each fund for your next meeting. That report gives you so much detail that you can shoot bullets into almost any fund as described below. (This same process can be used for insurance policies, stocks or any other financial instrument by using the relevant independent reports).

At the next meeting, I make enough space on my desk for two piles, labeled “sell” and “hold.”

I show the first Morningstar rating to the prospect. If the Morningstar Star rating is low, point out the rating. Explain to the prospect the rating system (5 great, 1 terrible). I often see people with 2 star funds. I explain the rating and explain that their fund is worse than average and ask them if we need to continue with more information about this fund. They usually say to me “sell that dog.” I place that page in the “sell” pile. If the rating is good, you still have plenty of data to show as follows.

the rating. Explain to the prospect the rating system (5 great, 1 terrible). I often see people with 2 star funds. I explain the rating and explain that their fund is worse than average and ask them if we need to continue with more information about this fund. They usually say to me “sell that dog.” I place that page in the “sell” pile. If the rating is good, you still have plenty of data to show as follows.

Point out the turnover. A Financial Analysts Journal article in 1993 calculated that 100% turnover was equal to a 1.2% fee (read Bogle on Mutual Funds by John Bogle). Additionally, high turnover creates short-term gains and taxes at ordinary income rates (rather than capital gain rates). You can then show the tax-adjusted return of the fund, which Morningstar also calculates. Even if the fund has performed well, you might ask the client “Were you aware that this fund, although it’s done okay, has caused you to lose almost 3% off of the return due to taxes each year? Would you like to see a solution (a low turnover fund that you recommend) to cut down those taxes?

Draw the prospect’s attention to the numbers on a Morningstar page showing the fund’s performance relative to its peer group and relevant index. Even though the fund may have done well, it might be a real laggard in its group and should be sold.

If you are a fee-based advisor, you will of course, disclose your fee. Then point out that by using your services, they will reduce their investment expense by using you. When you add up many funds management fee, 12b-1 fee and turnover impact, many funds are taking 3% to 5% of the account value, annually. Your fee, at say 1.25%, plus your recommended institutional fund fee of .2% is a huge bargain over what the prospect currently pays.

I have used these reports for years to gather ALL of the client’s assets because investors don’t really understand what they own and have most likely relied on some advisor's unsupported verbal recommendation. Additionally, it’s likely that no advisor has ever presented compelling third-party evidence for their recommendations. By the end of the meeting, I have a stack of Morningstar pages in the “sell” pile and the prospect asks me, “What should we do with this money?”(We also have a few selections that we continue to hold typically in a much smaller pile).

understand what they own and have most likely relied on some advisor's unsupported verbal recommendation. Additionally, it’s likely that no advisor has ever presented compelling third-party evidence for their recommendations. By the end of the meeting, I have a stack of Morningstar pages in the “sell” pile and the prospect asks me, “What should we do with this money?”(We also have a few selections that we continue to hold typically in a much smaller pile).

NOW, the prospect is ready for your recommendations because he has made the emotional decision to part with the items in the sell pile. If you skip the above unselling process, woe to you.

{kind=link}

[…] https://wealthyproducer.com/sales-professionals-must-unsell-before-they-sell/ […]